- Earned Income Tax Credits assist low- and moderate-income workers.

The federal and state Earned Income Tax Credits (EITC) are designed to boost earnings, especially among families with children, by reducing taxes or providing refunds to filers who do not owe taxes. To be eligible for the federal credit, parents must be ages 25–64, earn less than about $40,000 to $54,000 (depending on their filing status and number of children), and have limited income from investments. In addition, all family members on the tax return must have social security numbers. Childless adults must have incomes less than $15,000 to $21,000. The California EITC (CalEITC) augments the federal credit for low-income earners. First offered for tax year 2015, it was expanded in 2017 to include the self-employed and parents working full-time at the minimum wage. Eligibility thresholds are lower than for the federal credit: parents must have earnings less than about $22,000, while childless adults must have earnings less than $15,000. - Earned Income Tax Credits are among the largest social safety net programs.

In California, 3 million tax filers claimed $7.5 billion in federal EITC for the 2015 tax year, receiving on average $2,400. Of these, nearly 400,000 also claimed an average of $520 from the CalEITC, for a total of $200 million. Most EITC filers have dependent children, and more than 90% of total CalEITC claimed went to such families. Federal and state outlays on the EITCs were about the same as on CalFresh food assistance and more than twice as much as federal, state, and local expenditures on CalWORKs cash assistance. Following the recent expansion of the CalEITC, the 2017–18 state budget projects that an additional 1 million filers will be eligible for both credits in tax year 2017, upping total CalEITC benefits to $340 million. - Nearly one in seven Californians receive both state and federal credits.

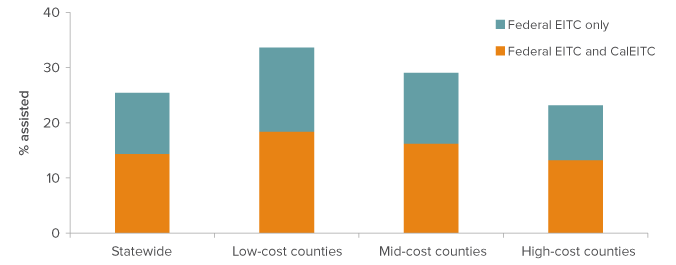

We estimate that 14% of Californians live in families assisted by both EITCs, and 9% more are assisted by the federal EITC alone. Californians in counties with low housing costs—where earnings are generally lower—are more likely to receive both credits. While there are no official data on eligible Californians’ rate of participation in the CalEITC, about 75% of eligible Californians claimed the federal EITC in 2014—somewhat less than the estimated rate in the nation as a whole (80%) but higher than state participation rates for both CalWORKs and CalFresh. Research indicates that most who are eligible for, but do not receive, the EITC fail to file a tax return in the first place, likely because their earnings are so low they are not required to file.

The federal EITC assists a quarter of all Californians

SOURCE: Author calculations using California Poverty Measure (CPM) data for 2013–2015.

NOTE: All estimates reflect EITC amounts imputed for 2017, using a baseline created in 2013–2015 data. This baseline incorporates a cost-of-living adjustment for the Supplemental Security Income (SSI) and CalWORKs programs, the 2017 minimum wage levels, and other adjustments. Low-, mid-, and high-cost counties were defined by splitting counties into three roughly equal groups based on CPM threshold. Statewide, the average CPM threshold over 2013–2015 for a family of four with two children is $31,019. In low-cost counties, it is $24,983; in mid-cost counties, $27,957; and in high-cost counties, $32,734. See Reducing Child Poverty in California for more details about the methodology.

- Earned Income Tax Credits help alleviate poverty across the state.

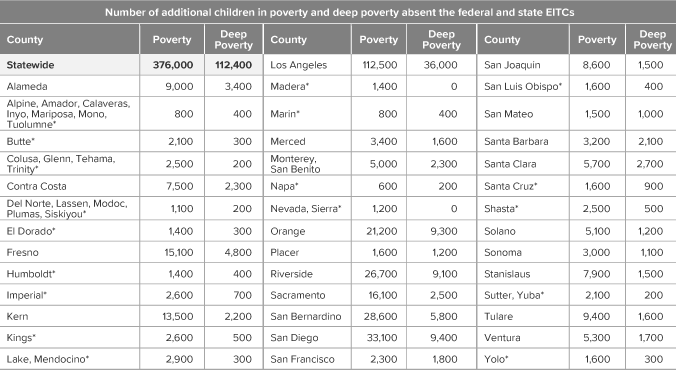

Without the federal and state EITCs, 840,000 more Californians (including 376,000 children) would be in poverty, according to the California Poverty Measure, which accounts for benefits from safety net programs. In addition, 275,600 more Californians (including 112,400 children) would be in deep poverty, with less than half the resources necessary to meet basic needs. Among large-scale safety net programs, the EITCs and CalFresh mitigate poverty and child poverty the most.

Without the EITCs, many more children would be in poverty and deep poverty

SOURCE: Author calculations using California Poverty Measure (CPM) data for 2013–2015.

NOTE: All estimates pertain to children ages 0–17 and use the baseline data described in the figure note above. Numbers are rounded to the nearest 100. Counties whose poverty rates cannot be calculated individually are grouped. All estimates are subject to uncertainty due to sampling variability; uncertainty is greater for less-populous counties and county groups because of smaller sample sizes. Asterisks indicate sample sizes under 2,000. For more about the CPM, see our fact sheet, “Poverty in California.” For more county-level information and for poverty rates by state assembly, state senate, and federal congressional districts, see our data page.

- Research indicates the EITC incentivizes work and improves health.

Studies have shown that major expansions in the federal EITC in the early 1990s encouraged employment, substantially augmenting the credit’s direct poverty reduction effect. The EITC may also have reduced the need for welfare assistance. Research has also suggested that this boost to earned income was responsible for better infant and maternal health outcomes and improved academic performance among children. - Outreach and expansion could amplify the effects of the EITC.

Intensifying outreach to non-filers promises to increase the effect of the CalEITC on its target population. Lawmakers may consider further expanding the CalEITC by raising earnings cut-offs, increasing amounts available to the lowest-income families, or both. They could alternatively consider additional tax credit designs. A recent PPIC report assesses the anti-poverty effects of several potential CalEITC expansions and alternative credits.

Topics

Economic Mobility Economy Health & Safety Net Jobs and Employment Population