- California’s largest public pension programs have significant unfunded liabilities.

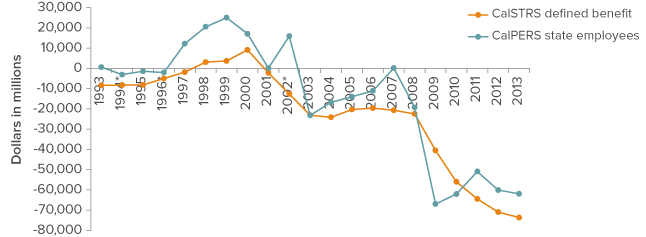

The state’s two largest public retirement programs, the California Public Employee Retirement System (CalPERS) and the California State Teacher’s Retirement System (CalSTRS), cover 65% of the four million state, county, and local employees who are eligible for public pension benefits. These two programs reported $62 billion and $74 billion in unfunded liabilities, respectively, for the 2013 fiscal year. An unfunded liability is a disparity between the estimated amount of a pension plan’s obligations and the current value of its assets. Over the past twenty years, CalSTRS’ unfunded liability has increased more than $65 billion and the CalPERS liability has grown by more than $63 billion. - Liabilities have grown even though average investment returns have been higher than expected.

Like many public pension funds, CalPERS and CalSTRS are long-term investors—their investments can be volatile in the short term but are expected to produce higher returns over a 20-year period. From 1993 to 2013, CalPERS and CalSTRS’ average investment returns were 8.57% and 8.46%, respectively—above the assumed rate of 7.5%. - Chronic underfunding and shifting state demographics have played a role.

The fact that liabilities have continued to grow even though average market returns have exceeded expectations suggests that the state pension systems have been underfunded over time. But shifting demographics are also a factor. The number of California adults age 65 and older has grown from 9% of the population in 1970 to 13% in 2013, and is projected to be as much as 17% by 2025. In the same period, birth rates have slightly declined, meaning that as the baby-boom generation ages there will be fewer younger workers to support the increasing number of public employee retirees. For many of these retirees, the state is also covering the cost of health care benefits.

California’s public pension systems are underfunded at historic levels

SOURCE: CalPERS and CalSTRS Actuarial Reports.

* CalSTRS unfunded levels for 1994, 1996, and 2002 were imputed.

- Recent changes to public employee retirement benefits have begun to reduce state costs.

In 2013, the legislature passed the California Public Employees’ Pension Reform Act (PEPRA, or AB 340), which reduced defined benefits, increased contributions for employers and employees, delayed retirement ages, and sought to eliminate practices that inflate benefits, such as large salary increases shortly before retirement. PEPRA also capped the amount of compensation used to calculate a defined benefit. AB 1469 increased school districts’ share of teacher-pension costs to 19% of payroll, an increase of nearly 11 percentage points over 7 years. In 2013–14 districts contributed about $2.1 billion to CalSTRS. This plan requires them to pay an additional $350 million in 2014–15 from Proposition 98 funding, with payments rising to $3.9 billion annually by 2020–21. - Unaddressed retirement liabilities could pose long-term risks to the state budget.

In general, unaddressed retirement liabilities grow at a faster rate than other state liabilities. While most budgetary liabilities are either fixed or have relatively low interest rates, unaddressed retirement liabilities result in the loss of investment returns, which compound over time and increase the cost of addressing the funding shortfall. The state could decide to increase contributions and set aside money in anticipation of higher costs as unfunded liabilities are paid off. Retiree health care is also a significant—and growing—liability. - Prefunding retiree health care could be an important step toward addressing growing costs.

Many of California’s public retirement plans offer health care benefits. The state pays for these health benefits on a “pay as you go” basis—each year, it covers the minimum amount of costs as they are due. State treasurer John Chiang has said that the current funding policy results in an additional $71.8 billion unfunded liability. Prefunding retiree health care involves significant costs, but it could dramatically reduce state costs in the future.

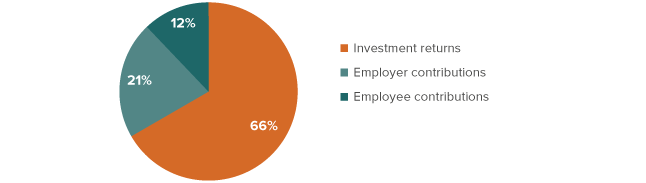

Two-thirds of CalPERS retiree benefits are covered by investment returns; retiree health care could be funded in the same way

SOURCE: CalPERS “Facts at a Glance,” 2013.

SOURCES: Legislative Analyst’s Office, Addressing California’s Key Liabilities (May 7, 2014). Pension funding and investment returns: CalPERS and CalSTRS Actuarial Reports. Health care: California State Controller’s Office, 2014.

Topics

PPIC News