This fact sheet analyzes data on undergraduate student loans in 2020, before student loan payments were paused in response to the pandemic.

Students often borrow to pay for higher education.

- US borrowers hold about $1.6 trillion in federal student loan debt; 3.8 million Californians owe over $142 billion of this debt.

- Subsidized and unsubsidized federal loans make up a majority (64%) of student borrowing, with Parent PLUS Loans, Grad PLUS Loans, Perkins Loans, and nonfederal loans combining to make up the rest.

- Just over half of all federal education loan dollars in the US in 2020–21 went to students pursuing undergraduate degrees.

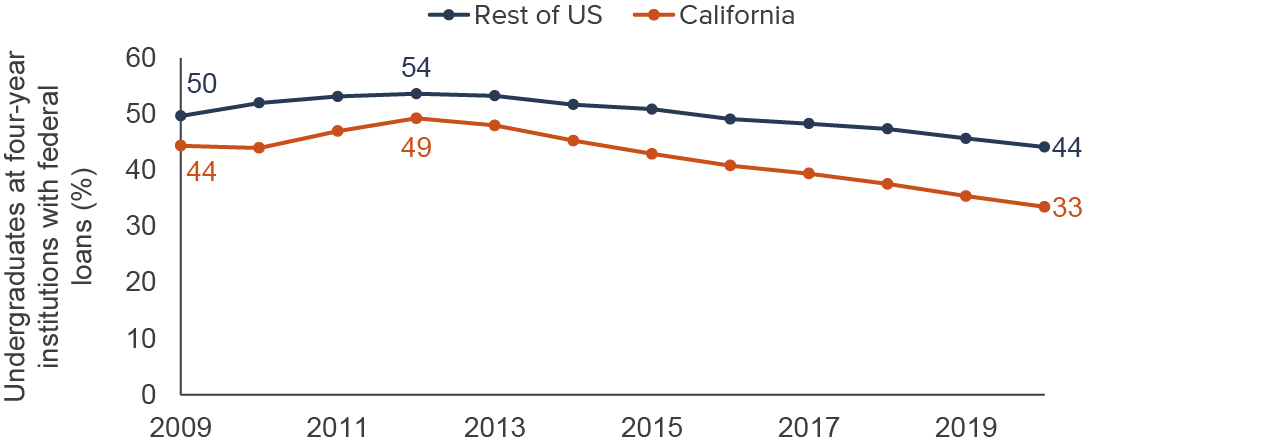

- Borrowing levels among undergraduates at four-year institutions nationwide decreased by 10 percentage points from 2012 to 2020. Borrowing rates in California, which have long been below the national average, dropped even more markedly; only one-third borrowed in 2019–20.

The rate of borrowing is declining and most students in California do not take out loans for four-year colleges and universities

NOTES: Figure shows data for four-year colleges and universities. Parent PLUS loans or private student loans are not included.

Undergraduate borrowing varies dramatically across systems and institutions.

- About 32% of undergraduates at the University of California (UC) take out federal loans. Median amounts of debt vary across campuses—from $13,200 at UC Davis to about $18,000 at UC Riverside.

- About 31% of California State University (CSU) students borrow, and the median debt upon graduation ranges from $13,200 (Cal State LA) to $25,000 (Cal Maritime). Students attending community colleges are very unlikely to take out federal loans.

- About 46% of students attending nonprofit private institutions borrow. Amounts vary dramatically, with Stanford University on the lower end (the median debt upon graduation is $12,000) and Southern California Institute of Architecture at the high end, with a median debt of $33,750.

- Over half of students (55%) borrow to attend for-profit institutions; their debt varies from a median of $3,200 for graduates of the two-year Coachella Valley Beauty College to a median of $45,000 at Design Institute of San Diego.

Some borrowers have struggled to repay their student loans.

- More than half of borrowers who attended UC and at least 40% of those who attended CSU and private nonprofits were making progress (lowering their principal balances) or paying off federal loans within the first three years. However, fewer than one in three borrowers who attended for-profit institutions were making progress. And, while borrowers who do not graduate usually accumulate less debt than graduates, they tend to struggle more to pay off loans.

- Prior to the pandemic, rates of loan delinquency (at least one missed payment) and default (nonpayment for over 360 days) were very low at public and nonprofit institutions. However, about one in four borrowers who did not graduate and about one in five borrowers from private for-profit institutions were in delinquency or default, which can reduce access to home and car loans or other types of credit.

- Additionally, about 18% of borrowers were making regular payments that were not large enough to shrink their principal balances. Another 38% of borrowers were in forbearance or deferment; these statuses can increase a borrower’s debt over time.

Rates of delinquency and default were higher among borrowers who attend for-profit institutions

NOTES: Figure shows estimates of the share of undergraduate federal student loan borrowers three years into repayment of each loan It does not include Parent PLUS or private student loans. Loans are delinquent after one or more missed payments; loans may be in in default after more than 360 days without payment.

Student loan payments are scheduled to resume soon.

- Student loan payments were paused after the pandemic began, but as a part of the recent debt ceiling deal payments will resume after August 30. However, defaults and delinquencies were erased in 2022, so all borrowers would start out in good standing.

- The Biden administration announced a debt relief plan last year that would cancel up to $10,000 in debt for borrowers with federal loans and up to $20,000 for Pell Grant recipients who meet certain income requirements. The plan faces political opposition and has been stalled by legal challenges that went to the Supreme Court.

- The plan would affect a majority (3.5 million) of borrowers in California, two-thirds of whom would be eligible for up to $20,000 in loan forgiveness.

- If the plan is implemented, loan forgiveness could cost the federal government about $30 billion per year for a total of about $379 billion.

Topics

Affordability Completion Higher Education Political Landscape