For the first time ever, the federal government has released data on loan debt for college graduates by type of degree and field of study. The data includes federal loans from three programs (Direct Loans, Federal Family Education Loans, and Graduate PLUS Loans) for students graduating in 2014–15 and 2015–16. This release is especially timely in light of national discussions about the cost of college–with some Democratic presidential candidates arguing for debt-free college and loan forgiveness. In just those two academic years, more than 300,000 Californians graduated from college (with degrees ranging from PhDs to vocational certificates) with debt. The total amount of federal debt among those graduates exceeded $10 billion.

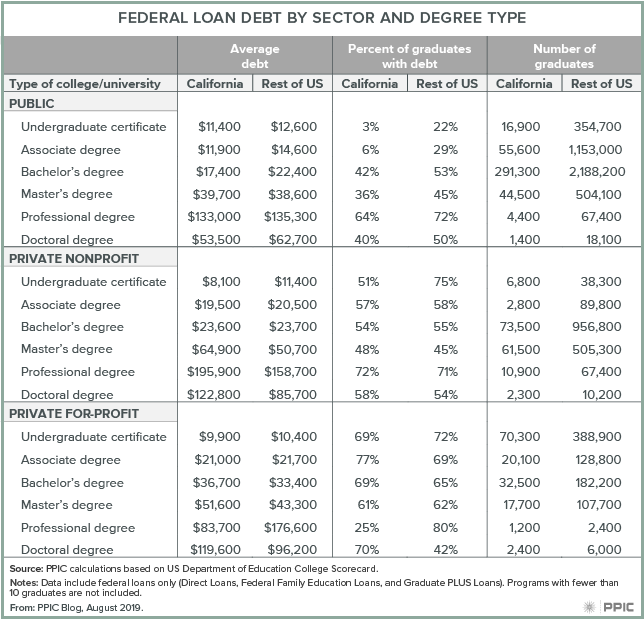

Some of the findings from the recently released data are not surprising. For example, undergraduates at public colleges and universities in California are less likely to take on debt than their peers in the rest of the country. And when students in California do take on debt, the amounts tend to be lower. Federal loan debt for Californians earning bachelor’s degrees at UC and CSU averages $5,000 less than at public universities in the rest of the country ($17,400 versus $22,400). And undergraduates in California are less likely to take out federal loans (42%) than their peers in the rest of the country (53%). Only 6% of associate degree holders from the state’s community colleges have federal loans, compared to 29% of public community college graduates in the rest of the country. Students at California’s public colleges and universities are also less likely than their counterparts at the state’s private institutions to take on debt, and those who do take out loans graduate with less debt.

Other findings are striking. In California and the rest of the nation, graduate students tend to have far higher loan amounts than undergraduates, with professional degree holders incurring the most debt—generally well over $100,000. The most common professional degrees are in law, medicine, and dentistry. Graduates of professional schools at private nonprofits in California incur the most federal loan debt—almost $200,000. In general, graduate students at California’s public universities are less likely to take on debt, and their loan amounts are lower than those for students at private colleges. Even so, graduate students at public institutions are incurring large amounts of debt.

Large debt levels among graduate students reflect higher tuition for many programs. For example, tuition and fees at UC Berkeley’s law school are almost $60,000 for 2019–20, compared to less than $20,000 for academic graduate programs such as English. High demand for many graduate professional programs coupled with expectations of earnings premiums account for both the higher tuition and students’ willingness to take on debt.

Policies to address student debt must be mindful of which students take on debt, the range of institutions and areas of study, and the ability of students to pay back their debt. These are critical concerns in putting college graduates on the path to economic mobility and long-term financial security.