Key Takeaways

In recent years, some high-profile companies, like Tesla and Chevron, have moved their headquarters out of California, making headlines and raising concerns about the state’s economic future. Are these anecdotes indicative of a broader trend? What is the impact on jobs when headquarters leave the state? Do headquarter relocations reveal anything about California’s underlying business climate?

In this report, we study these questions by examining headquarter relocations from California and nationwide using comprehensive data on all business establishments. We find:

- The number of firms whose headquarters have left the state is small. From 2011 to 2021, 1.9 percent (789) of the state’s more than 47,000 headquarters left California on net. The decrease in jobs resulting from these relocations represented 3.7 percent (about 77,600) of all headquarter jobs. Roughly half of the headquarters that left California were in manufacturing, wholesale trade, or business services. →

- The annual number of relocations has trended upwards. About 150 headquarters left California in 2011, compared to over 200 in 2021. Over this time period, headquarter relocations from other states to California declined from almost 140 to just under 70. Headquarters that leave California tend to go to other large states like Texas, New York, and Florida, or to nearby states like Nevada and Arizona. →

- Headquarters that move out of state keep other branches and jobs in California. Further, companies that move headquarters to other states do not appear to shrink non-headquarter employment in the state relative to firms whose headquarters stay in California. Job loss due to relocation appears mostly limited to headquarter jobs. →

- California headquarters that relocate tend to go to states with lower taxes and less regulation. The same pattern is evident among headquarters relocating nationally. Over the period studied, California did not reduce tax and regulatory burden as much as other states—a potential reason behind the uptick in headquarters leaving the state. →

- Relocations are a small fraction of overall headquarter activity. Between 2011 and 2021, far more headquarters launched (7,250, 17% of companies headquartered in California) and closed (12,700, 30%) than moved out of state, with no clear upward or downward trends. Focusing solely on relocations overlooks the range of positive and negative forces driving headquarter activity and can misrepresent businesses’ desire and ability to operate headquarters in California and the broader impact on jobs. →

While California has high taxes and tough regulations, it also boasts a highly educated and innovative workforce, a good climate, and quality-of-life amenities that can both attract and retain businesses. It is too early in our research agenda to make firm policy recommendations, but a broad and simple lesson is that the state should continue to examine ways to maintain or strengthen the features that make it attractive to headquarters (and businesses more generally) while critically evaluating the costs and benefits associated with policies that may be causing headquarters to leave.

Introduction

In the last few years, some major companies headquartered in California have left the state, including Tesla moving its headquarters from Palo Alto to Austin, Texas, and Chevron moving from San Ramon to Houston, Texas. While these events garnered headlines, a handful of businesses moving their headquarters out of the state is unlikely to move the needle on California’s $3.9 trillion economy. However, these high-profile relocations have naturally raised concerns about the business climate in California:

- First, it is possible that high-profile relocations reflect a broader pattern among businesses, many of which might not make headlines. These prominent cases could be the proverbial “canary in the coal mine,” indicating an overall decrease in California’s ability to attract and sustain headquarter operations—or businesses more generally.

- Second, headquarter relocations affect jobs. These decisions most immediately affect the high-paying jobs that tend to be housed at headquarters. In addition, headquarter relocations may influence broader business decisions about employment at branches both in and out of California. Headquarter relocations thus have implications for state tax revenue, which relies heavily on high-income earners, and may also have implications for job growth more generally in California.

The fact is that companies, headquarters, and branches are always entering and leaving states, as well as launching, growing, or shrinking. Businesses must consider many different factors when making these decisions. When it comes to location, California does have high taxes and tough regulations, which could potentially make other states attractive destinations. But the state boasts key advantages as well, including highly educated and innovative workers and population density, both of which can make businesses more productive. The state also offers a good climate and appealing quality-of-life amenities, including its environment, natural beauty, and rich and vibrant culture. While California’s high housing costs may negatively affect some companies and factor into location decisions, these high costs could also reflect some of the benefits the state offers to businesses and their workers.

In this report, we look beyond the anecdotes to provide systematic evidence on statewide changes in headquarter moves and the implications for employment. We assess not only headquarters that relocated out of California but also those that moved to California, as well as those that launched or ceased operations in the state. To provide this detailed picture, we draw on new longitudinal data that we have compiled covering all business establishments nationwide (see textbox).

The purpose of this report is descriptive, namely, to understand the trends in headquarter relocations, and to assess potential drivers of these trends to assist policymakers as they consider ways to incentivize businesses to remain in the state. This report begins by tracking trends in headquarter relocations in California, including associated jobs and sectors. We then examine relocation patterns to other states and how destination states differ from California (and each other) in terms of taxes and regulations, education levels, and housing prices. Next, we present broader headquarter and employment dynamics, including trends in employment at California branches and headquarter launches and closures in California. Finally, we conclude by discussing the broader implications of our findings.

Overall Trends in Headquarter Relocations

In this section, we provide an overview of patterns in headquarter relocations from 2011 to 2021, including the size of the headquarters that left the state, the associated number of headquarter jobs lost, and trends across sectors.

Headquarter Relocations Are Increasing

In total, over 49,000 companies are headquartered in California as of 2021, across all sectors of the economy. Some companies headquartered in the state are well-known global brands like Apple, Alphabet (Google), and Tesla, but many more are not household names.

Companies with headquarters in California are significantly larger than other businesses in the state. These companies have an average of 97 employees in California, including employees at headquarters and other branches. In contrast, companies without multiple branches employ an average total of five employees. Further, California headquarters themselves are larger than their non-headquarter branches in the state, with an average of 50 employees compared to 33. Meanwhile, California branches of companies that are headquartered outside the state average 27 employees.

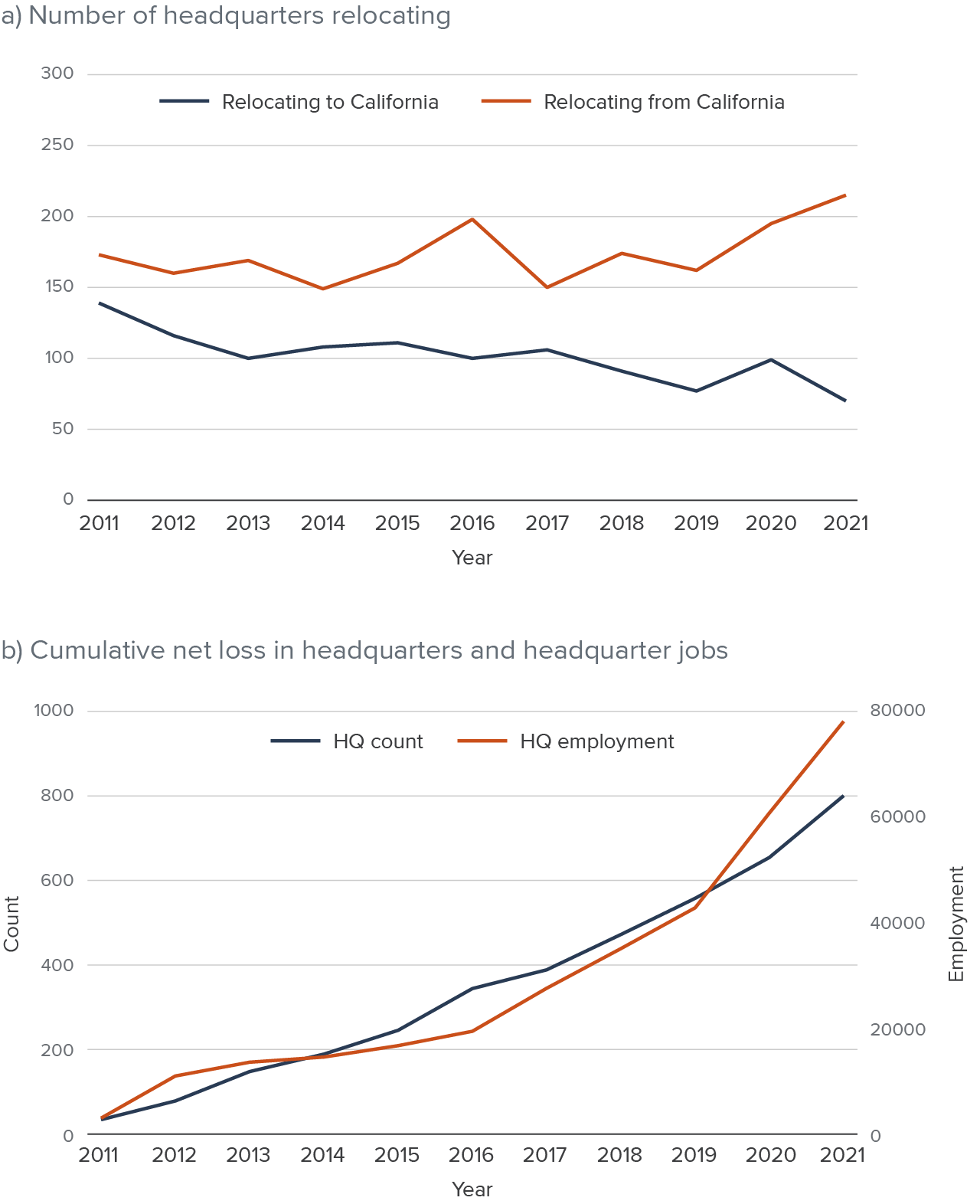

Our data track employment in each establishment of each firm and changes in the location of any branch and headquarters. Figure 1a shows changes in headquarter locations. From 2011 to 2021, between 147 and 213 companies moved their headquarters out of California each year, with an upward trend in the outflow since 2017, reaching the highest levels seen in the ten-year period under review. During this time, fewer companies moved their headquarters from other states to California, and this number declined, from 137 in 2011 to 68 in 2021.

Figure 1b shows the cumulative number of headquarter relocations (left-side axis) and the associated cumulative employment changes based on employment at headquarters just prior to the move (right-side axis). On net, accounting for exits and entries, the cumulative loss from 2011 to 2021 was 789 California headquarters and 77,569 headquarter jobs.

Companies headquartered in California are increasingly moving out of state, and jobs are leaving with them

SOURCE: Authors’ analysis from Mergent data, 2010–2021.

NOTE: For each year, we measure moves between the given year (shown in chart) and the prior year in our data; for example, the 2011 data point represents headquarters that moved sometime between 2010 and 2011. We measure employment as of the prior year in the original location as an estimate of the job loss.

In summary, the systematic data we analyze indicate an increase in headquarter exits from California and consequent loss of headquarter jobs. To put the magnitude of these changes in context, the number of headquarter relocations cumulatively represented about 1.9 percent of the state’s headquarters in 2010 (41,715 firms were headquartered in the state at that time). Meanwhile, the jobs at these headquarters—now located out of state—were 3.7 percent of all headquarter jobs in 2010. We can also put the jobs lost from (net) headquarter exits in the context of overall employment changes: they represented 2.6 percent of the jobs added in California over the period (non-farm employment grew by 3.1 million between January 2010 and December 2021).

How important these changes are is a subjective matter. We imagine that virtually any reader or policymaker would prefer that these headquarters and jobs had not left California. We do not think these changes should be viewed as negligible, but at the same time, in our assessment, these changes in headquarter business dynamics do not reflect major changes in the state’s employment picture (see text box for earlier research on California business relocations).

Larger Companies Are More Likely to Move Their Headquarters

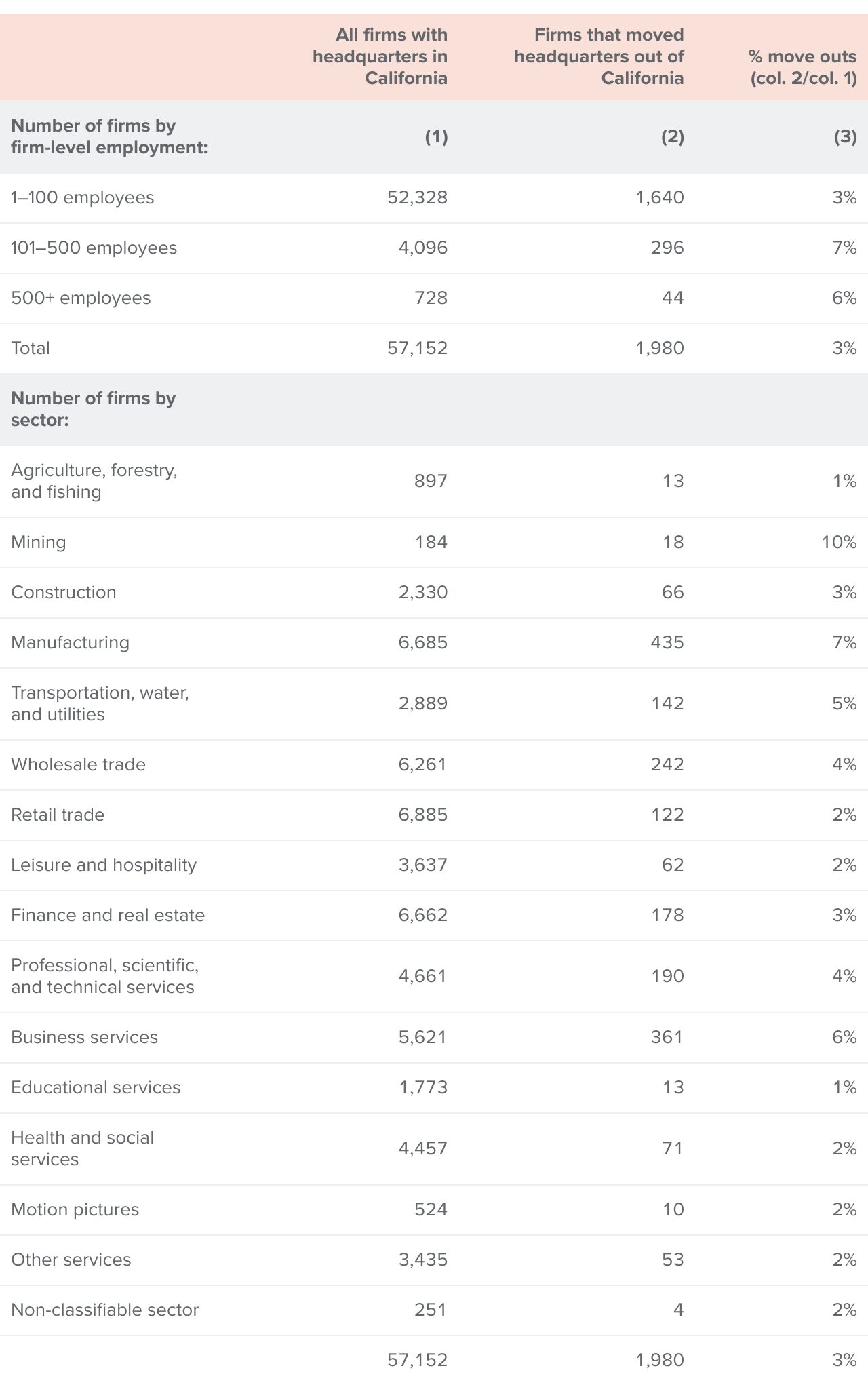

Headquarters exiting the state are larger than average, meaning their exits have a disproportionate impact on jobs. As noted above, headquarter exits constituted 1.9 percent of headquarters based in the state in 2010, but 3.7 percent of employment at those headquarters.

In addition, headquarter relocations were concentrated among larger companies generally. In particular, an outsized share of relocating headquarters (17%) had over 100 employees total in the company, compared to all businesses in the state (8%). Similarly, as shown in Table 1, companies with 101–500 employees and over 500 employees were more likely to move out of state than those with 100 or fewer employees (7%, 6%, and 3%, respectively).

When we examine patterns across industries, we find the following sectors had the largest number of headquarter relocations: manufacturing (435 headquarter relocations), wholesale trade (242), and business services (361). These large sectors made up 52 percent of relocations between 2011 and 2021, and rates of relocation were higher in these sectors than other sectors (third column). Notably, some other large sectors, such as retail trade, and finance and real estate, had relatively low rates of relocation over this period. Headquarter relocation rates were particularly low in retail trade, health and social services, educational services, motion pictures, and agriculture.

Headquarter relocations are concentrated among larger companies and certain sectors

SOURCE: Authors’ analysis from Mergent data, 2010–2021.

NOTES: Table counts all unique firms that were headquartered and operated in California between 2010 and 2021. To be defined as a firm headquartered in California, the firm must have more than one establishment and an establishment in California identified as the firm’s headquarters. These firms may have started, closed, or relocated within the time period. Sector classification is based on 4-digit SIC codes at the firm’s first appearance in the data, except in cases where the SIC code was initially “non-classifiable,” in which case we “backfilled” from a later code when available (see Technical Appendix A). We aggregate SIC codes to the categories in the table (see Technical Appendix Table A3 for details). Employment numbers are the average non-missing values between 2011 and 2021. Employment counts all of the firms’ California locations.

Where Do Exiting Headquarters Go?

In this section, we examine the characteristics of destination states for headquarters that leave California, with a particular focus on whether taxes/regulations, education levels, and housing prices are associated with headquarter exits. We also investigate whether nationwide patterns resemble those for headquarters moving out of California.

Exiting Headquarters Often Choose Large or Close Destination States

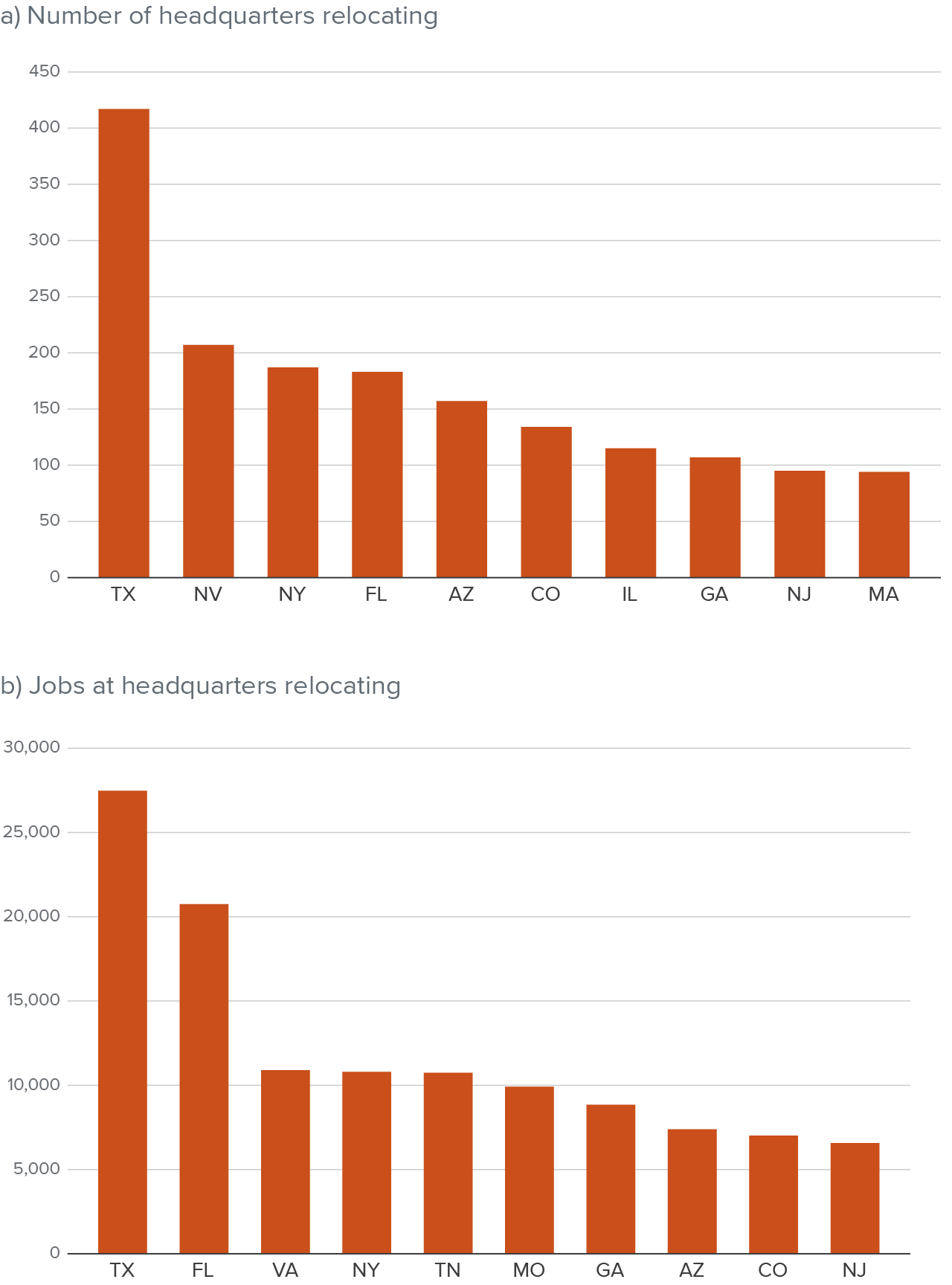

Headquarters that leave California tend to go to other large states like Texas, New York, and Florida, or to nearby states like Nevada and Arizona. The same is generally true of the corresponding job relocations (Figure 2). Overall, about two-thirds of the headquarters that left California went to these five states. The fact that many headquarters relocated to large states is not surprising since large states have more economic activity. Moves to close locations are also to be expected because of how smaller distances affect business costs like transportation and travel.

Headquarters that relocate from California tend to move to large or nearby states

SOURCE: Authors’ analysis from Mergent data, 2010–2021.

NOTE: Figures show top 10 destination states for headquarter relocations out of California, based on the cumulative number of headquarters (panel a) and the cumulative number of jobs at headquarters (panel b). Relocations into California are not considered in this chart.

Exiting Headquarters Tend to Choose States with Lower Taxes and Less Regulation

In addition to size and proximity, other factors that could influence relocation decisions include the cost of doing business due to the tax or regulatory environment, the ability to find workers with the necessary skills and training, and the cost of hiring as influenced by housing prices or income tax rates faced by workers. Below, we examine whether these factors play a role in headquarter relocations, first in California and then nationwide.

In our analysis, we rely on established measures of taxes and regulations, education levels, and housing costs to compare where states fall on each dimension (see textbox for more detail). On these metrics, California ranks as follows:

- Taxes and regulations. California has relatively high taxes and strong regulations compared to other states. Using the Fraser Institute’s “Economic Freedom Index”—but reversing it so that a high value reflects high taxes and more regulation—California ranked the second highest (after New York) in 2010, right before the beginning of our analysis period.

- Education levels. California is in the middle (22nd) nationwide when it comes to the population’s average education level (the top two states are Massachusetts and Maryland), based on the Information Technology and Innovation Foundation’s workforce education score.

- Housing costs. California has the third-highest housing costs in the nation, behind Hawaii and Massachusetts, based on Zillow’s Home Value Index.

California Patterns

To describe how these factors relate to headquarter relocations, we begin by examining all headquarter exits from California between 2011 and 2021, and how the destination states vary in terms of the tax and regulatory environment, workforce education levels, and home prices. Specifically, we estimate regression models that allow us to quantify which traits of destination states do the most to explain headquarter exits from California to those states. We also control for distance to the destination state and the size of the destination state’s economy. We run models separately to explain the number of headquarter moves from California and the number of jobs at headquarters that move.

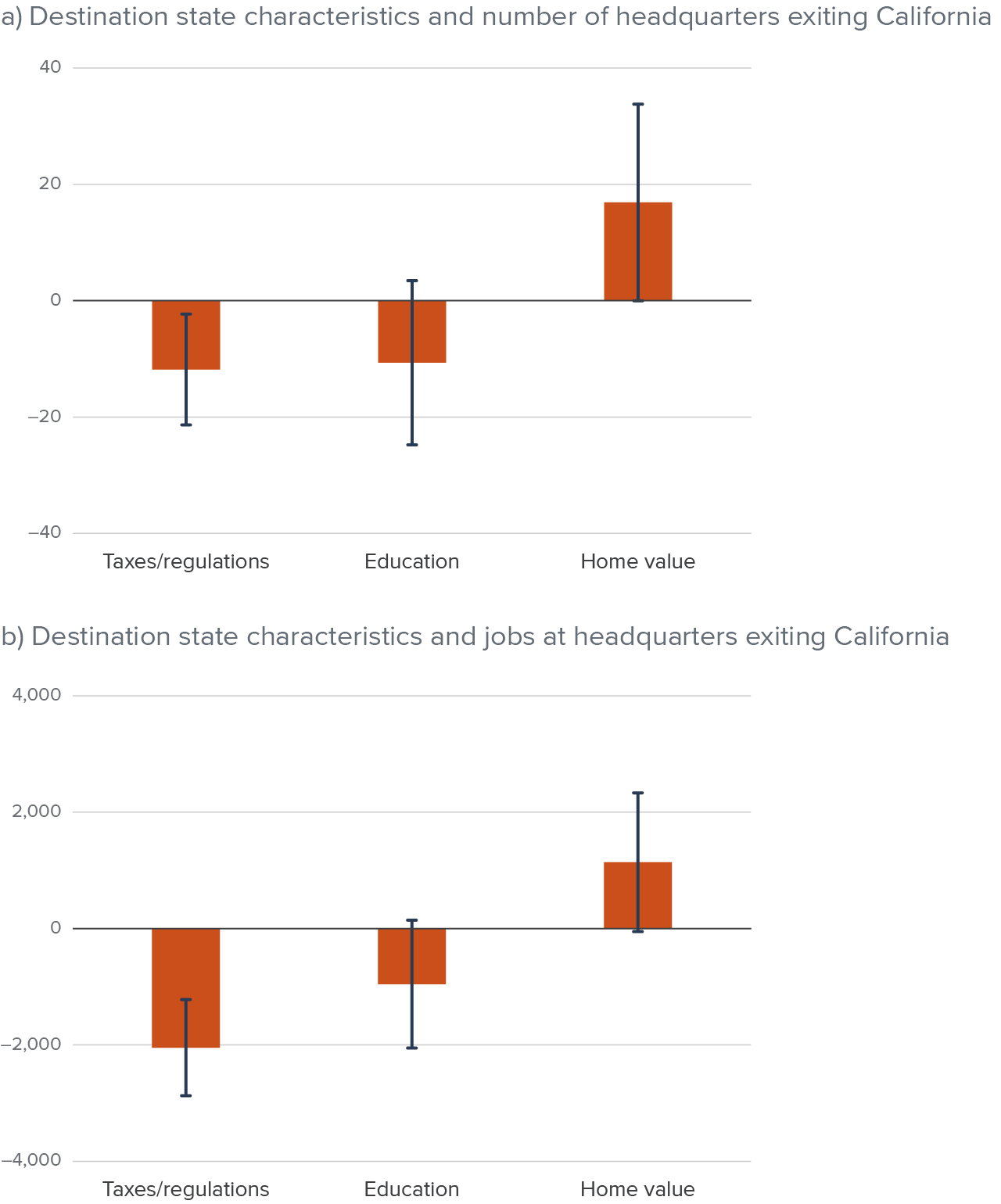

We find that California headquarters tend to move to states with lower taxes and less regulation (Figure 3). This holds for the number of headquarters leaving California and employment at these headquarters. Specifically, we estimate that a state ranked about 20 places higher, with more taxes and regulations than an otherwise similar state, will have 11.8 fewer headquarter relocations to that state.

Meanwhile, education demonstrates a similar negative relationship (higher workforce education is associated with fewer headquarter relocations to that state), but it is not statistically significant. California headquarters are more likely to move to states with higher real estate prices, but again that relationship is not statistically significant. We come back to these latter two findings later.

Headquarters leaving California tend to choose states with lower taxes and less regulation

SOURCE: Authors’ analysis from Mergent data, 2010–2021.

NOTE: Figures show coefficients (bars) and 95 percent confidence intervals (lines) from regression models of headquarter relocation out of California to destination states. Each unit is a destination state (other than California). The dependent variable is the headquarter count (panel a) and associated jobs (panel b) for headquarter moves from California to each of the 49 other states. The independent variables are explained in the text box below. Each variable is rescaled with a standard deviation of one, so the estimated bars reflect the effect of a one standard deviation change in the index. Coefficients less than zero indicate a lower likelihood of moving to a state with higher taxes/regulations, workforce education, and home values, respectively. See Technical Appendix Table B3 for regression model estimates and related statistics; the estimates reported in Figure 3 are from columns (1) and (3) of Table B3.

Nationwide Patterns

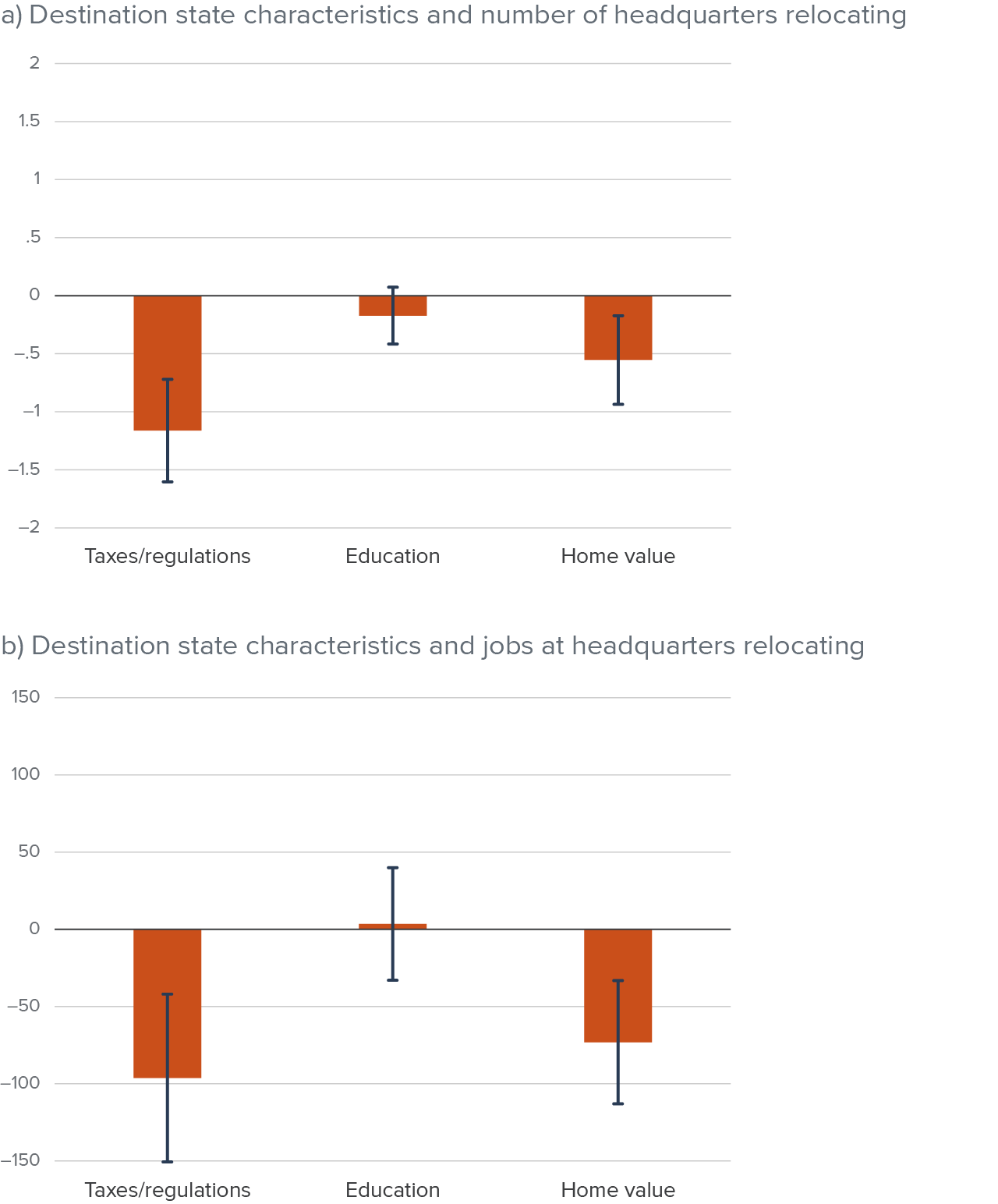

The nationwide patterns for headquarter relocations are similar to the results for California headquarters alone (Figure 4). In particular, headquarters that relocate tend to move to states with lower taxes and less regulation. Across all states, headquarter relocations seem uncorrelated with average education in the workforce (coefficients are small and insignificant).

When it comes to real estate, headquarters nationwide tend to move to states with lower housing prices—in contrast to our findings for California headquarters, where the estimate of housing prices goes in the opposite direction (but was not a statistically significant factor). One potential reason for this difference is that housing prices are both a cost of doing business (i.e., something viewed as a negative by businesses because workers will regard the cost of living as higher) and a reflection of highly productive workers and businesses because land prices are higher where businesses and workers are more productive. That is, housing prices can be an advantage to businesses as well as a “cost” (Roback 1982), and the extent to which housing prices reflect one or the other may vary across states. For example, in California, high housing prices may be more reflective of productivity differences and not just business costs. In contrast, a state’s tax and regulatory environment may be a more independent, longer-standing feature of state business climates, which could explain why the results for this index are similar when we examine headquarter exits from California (Figure 3) and all moves nationwide (Figure 4).

Nationwide, headquarters tend to relocate to states with lower taxes/regulations, higher education levels, and lower housing prices

SOURCE: Authors’ analysis from Mergent data, 2010–2021.

NOTE: Figures show coefficients (bars) and 95 percent confidence intervals (lines) from regression models of relocation of headquarters between states. Each unit is a pair of origin and destination state (N=2,450). The dependent variable is the headquarter count (panel a) or employment (panel b) moving from the origin state to the destination state. The independent variables are explained in the text box above. We include the differences between destination state and origin state for each index. The indices are rescaled with a standard deviation of one before differencing. Coefficients less than zero indicate a lower likelihood of moving to a state with higher taxes/regulations, workforce education, and home values, respectively. See Technical Appendix Table B4 for regression model estimates and related statistics.

California Has Not Reduced Taxes and Regulations as Much as Other States

Overall, strong and consistent national and California patterns of headquarter relocations suggest that places with lower taxes and less regulation have some advantages in retaining and attracting headquarters. Note, though, that this analysis does not answer the question of whether changing any of these factors increases retention of headquarters to a particular place or attracts headquarter relocations. Specifically, we do not at this point evaluate whether policy changes in California led to the increase in headquarter exits. Future work could attempt to pin down causal relationships by isolating specific policy changes and measuring whether there are resulting headquarter relocations.

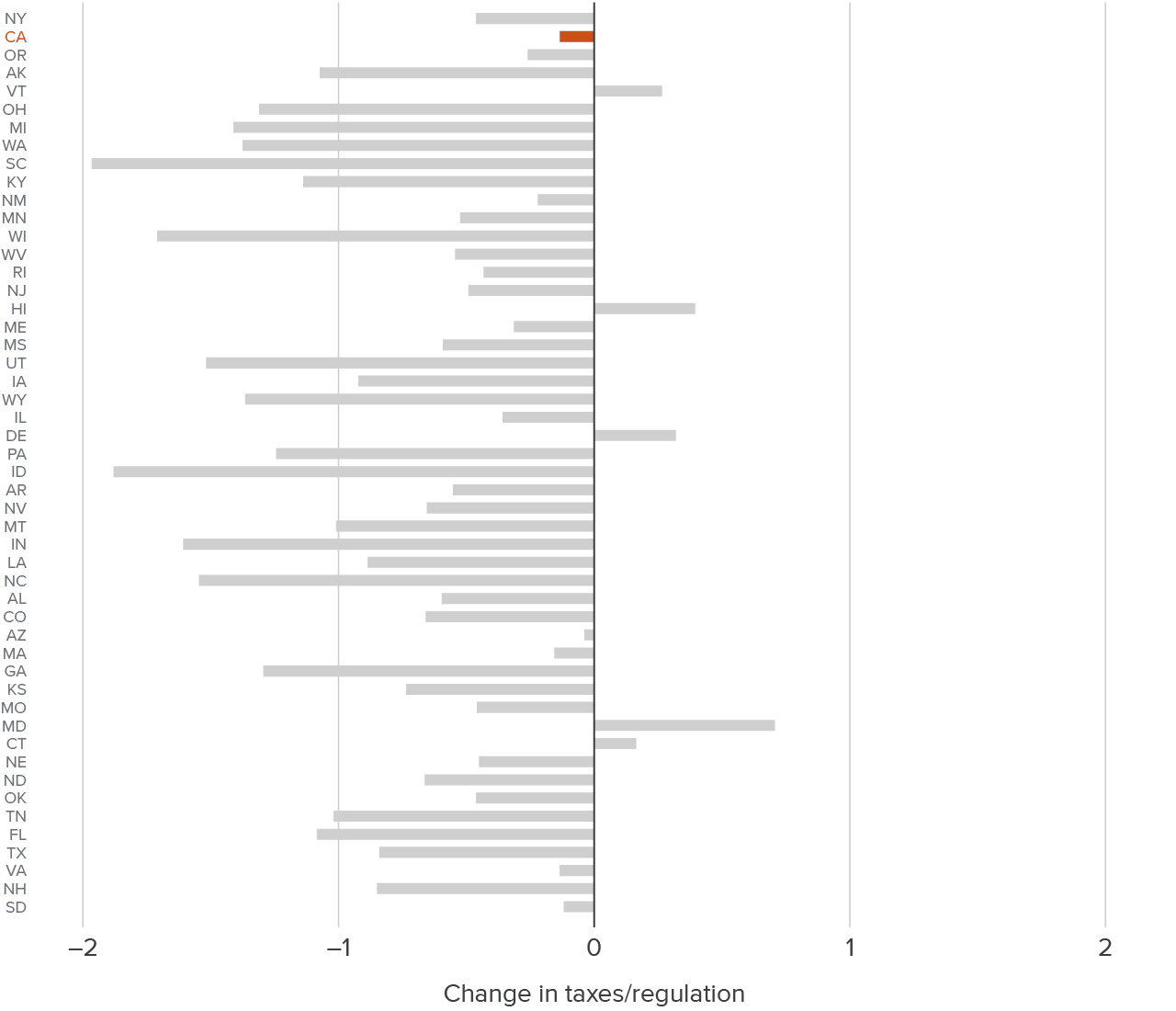

That said, California has lagged behind most states in terms of reducing tax and regulatory burden as captured by the tax and regulation index. Figure 5 displays the changes in tax and regulatory burden across states from 2010 to 2021, with the states at the top of the chart having the highest burden as of 2010 (as noted earlier, California was ranked second highest in terms of tax and regulatory burden, after New York). Most states show substantial negative changes, implying a lowering of taxes and regulations. In contrast, California shows only a modest reduction. It is possible that this relative change helps explain the uptick in headquarter exits from California.

Between 2010 and 2021, California had a small decrease in tax and regulatory burden compared to other states

SOURCE: Fraser Institute: Economic Freedom Index of North America (2010, 2021).

NOTE: States on the vertical axis are ranked by their taxes/regulations (from highest to lowest) in 2010, where the bars represent their change in taxes/regulations between 2010 and 2021.

Broader Headquarter and Employment Dynamics

As shown above, there has been an increase in headquarters leaving California. This rise in headquarter exits could be a “canary in the coal mine,” warning of problems with the continued viability of headquarter operations in the state. It could even indicate broader challenges to employment, with corporate exits being the tip of the iceberg. In this section, we develop a fuller understanding of changes in headquarter operations and the employment changes associated with headquarters leaving the state.

First, we examine if headquarter exits affect employment at these companies more generally. Does employment at other branches tend to flow out of the state when headquarters leave? If so, then headquarter exits suggest a bigger problem for employment in the state.

Second, we study the overall “health” of headquarter operations in the state. Many businesses are headquartered in California and have not left. Headquarters can close altogether, open in the state, or move to California from other states. Before concluding that relocations indicate a less hospitable environment for headquarter operations, we need to first examine these other dynamics.

Employment at California Branches Appears Unaffected

Following a headquarter relocation from California, there is little to no impact on non-headquarter employment in the state (Figure 6). This analysis controls for when a headquarter moved (given business cycles from 2010–2021), industry patterns of relocation, and trends among California companies that did not relocate. While there is a small initial increase in non-headquarter employment followed by a decrease, this pattern is not statistically strong and is by and large consistent with no change.

There is little impact on employment at other branches when company headquarters leave California

Average effect on non-HQ employment

SOURCE: Authors’ analysis from Mergent data, 2010–2021.

NOTE: This chart presents point estimates (dots) and 95 percent confidence intervals (capped lines) from a two-stage difference-in-differences event study model. The horizontal axis reflects the year relative to the firm’s year of relocation, where -5 and 5 indicate “five years and before” and “five years and beyond,” respectively. The reference year is the year prior to the relocation (-1). The dependent variable is non-headquarter (HQ) employment. We account for firm, year, and industry-year fixed effects.

Exits Are a Small Fraction of Headquarter Activity

Finally, we turn to broader dynamics of company headquarters—not just relocations. As noted above, the 789 headquarters that left California on net between 2011 and 2021 constituted 1.9 percent of the base headquarter count in the state in 2010. However, it also important to consider headquarter closings, which, like exits, represent lost headquarter employment in the state, and headquarter openings, which come with gains in employment.

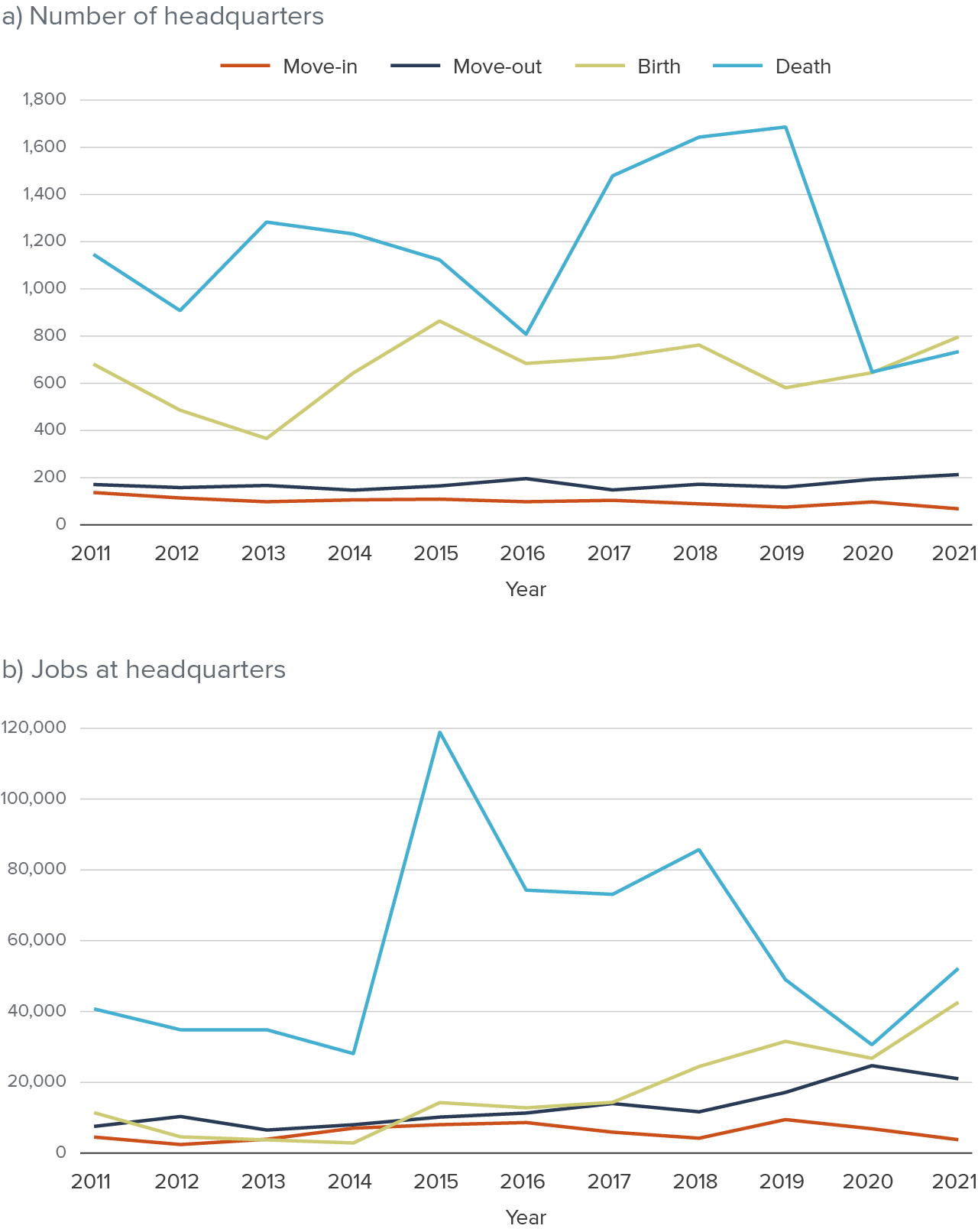

As shown in Figure 7a, between 2010 and 2021, roughly 7,250 headquarters opened in California, and nearly 12,700 closed. Those activities represented 17 percent and 30 percent, respectively, of all headquarters in 2010, much larger shares than the percentage that relocated. Moreover, the level of headquarter births has not declined. These numbers make three points.

- Closings exceeded exits, suggesting that a sole focus on exits as a negative indicator of the state’s business environment is incomplete.

- There were far more new headquarters than headquarters that exited the state. A narrow focus on exits misses a positive aspect of headquarter activity in California.

- While headquarter relocations made headlines, they constituted a very small part of the overall “health” of business headquarters in California.

Based on Figure 7a, we might conclude that exits and entries are not very relevant because they occur at a much lower rate than births and deaths. However, Figure 7b reminds us that the employment levels at headquarters undergoing these different changes vary quite dramatically. In particular, new headquarters are always small, so the initial jobs gained from new headquarters are relatively low, though still higher than the change due to relocations (3.7%). The increase due to headquarter openings represented 9 percent (about 189,500) of all headquarter jobs from 2011 to 2021. In contrast, closing headquarters tend to be quite large, with considerable job losses. The decrease due to headquarter closures represented 29.7 percent (622,400) of all headquarter jobs over the period studied.

Perhaps less predictable is that the employment levels at headquarters that exit are larger than those of headquarters that move in (a function of increasing exits but also the size of the headquarters). This is especially true in the later years and suggests that the job loss from headquarter exits warrants more serious attention than just focusing on headquarter counts would indicate. Job loss from headquarter exits was similar to job changes due to headquarter births (and in some years deaths) despite being much smaller in number. This reinforces our conclusion that headquarter exits are just one part of the dynamics of headquarters in California, that job loss from headquarter exits are neither negligible nor major, and that some aspects of headquarter dynamics remain favorable for the state.

Relocations represent a smaller portion of headquarter activity than new and closing headquarters, but employment at relocating headquarters is higher

SOURCE: Authors’ analysis from Mergent data, 2010–2021.

NOTE: For each year, we measure changes between the given year (shown in chart) and the prior year in our data; for example, the 2011 data point represents headquarters that moved, started, or closed sometime between 2010 and 2011. We measure employment as of the prior year, except for headquarter births.

Conclusion

High-profile companies moving their headquarters out of California have raised concerns about the state’s future as an economic powerhouse and its ability to attract and retain businesses. In this report, we go beyond the headlines to study headquarter relocations using comprehensive data on all business establishments.

We find that the number of companies whose headquarters have left the state is small relative to all businesses headquartered in California (1.9%). However, the number of headquarters exiting the state has risen from about 150 leaving in 2011 to over 200 in 2021. Meanwhile, headquarter relocations from other states to California declined from almost 140 to just under 70.

Fortunately, the impact of headquarter relocations on employment appears mostly limited to headquarter jobs. Headquarters that leave California mostly keep some branches and jobs in the state, and they do not generally shrink non-headquarter employment in California relative to companies whose headquarters stay in the state. This finding is perhaps not surprising given California’s population density, which provides a large labor market and a robust customer base for goods and services.

Moreover, the continued high rate of headquarters launching in California suggests that the state still retains advantages for establishing company headquarters. Between 2011 and 2021, far more headquarters were launched in the state than moved out of state, although new headquarters tend to have many fewer jobs at the outset. Regardless, even though headquarter relocations do not constitute a large outflow of jobs, and there are other favorable headquarter dynamics in California, the state would be better off if fewer companies relocated their headquarters out of state, all else being equal.

We find that headquarter relocations out of California most often go to large states like Texas, New York, and Florida, or nearby states like Nevada and Arizona. Exiting headquarters also tend to choose states with lower taxes and regulation, indicating that these factors could be important for businesses. Over the period studied, California did not reduce its tax and regulatory burden as much as other states—a potential reason behind the uptick of headquarters leaving California. Headquarter relocations nationwide reflect the same pattern with respect to taxes and regulation, while also suggesting that housing prices matter for destination choice. Neither education levels nor housing prices appear to be significant factors for headquarters relocating from California.

Some aspects of business conditions are more amenable to policy action than others. For instance, regulation and tax rates are directly set by governments, but housing costs and educational attainment of the population are, though influenced to some extent by government policy, also shaped by individual and societal forces. Moreover, government policy in these and other areas encompasses a host of goals and tradeoffs beyond those affecting business conditions, meaning policymakers must weigh any potential benefits to businesses against other considerations.

As policymakers continue to consider ways to attract and retain businesses, it will be important to continue digging beyond the basic headlines and to understand the underlying causes of the patterns that emerge. Such efforts are necessary to ultimately identify effective policy options for creating an environment that is conducive to business and job growth and retention.

Topics

Economic Trends Economy Jobs and EmploymentLearn More

California’s Businesses

Business Regulation and Business Starts in California

Experts Answer: Are Headquarters Really Fleeing California?

Priorities for California’s Economy

Business Climate Rankings and the California Economy

Are Businesses Fleeing the State? Interstate Business Relocation and Employment Change in California